In today’s environment of low interest rates, many investors are chasing income by moving into lower-quality high-yield bonds, but are they ignoring the downside risks?

While an overweight to high-yield credit may be an efficient way to boost a portfolio’s yield, investors need to be mindful of the additional risks they are taking on and how those risks will interact with other parts of their investment portfolio.

For example, for retirees seeking a stable income-generating portfolio, the addition of less-liquid bonds that have an increased risk of capital volatility might not be the right investment option, despite the income they produce.

Here, we explore the different types of fixed income securities and their associated risks.

Types of fixed income securities

The types of fixed income securities investors can choose from include both publicly-traded debt securities (such as corporate bonds, sovereign and non-sovereign government bonds, supranational bonds, and commercial paper) and privately-traded instruments (such as loans and privately placed securities). The credit market also includes structured financial instruments, such as mortgage-backed securities, asset-backed securities, and collateralized debt obligations, which tend to exhibit higher yields (and lower liquidity) as the complexity increases.

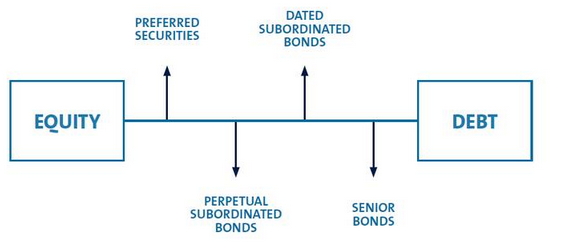

Within corporate bonds, there are several classes of debt, ranging from senior bonds to preferred securities. Senior bonds have greater security in the issuer’s capital structure than subordinated debt and preferred securities. In the event the issuer goes bankrupt, senior debt must be repaid before other creditors receive any payment. Senior debt is often secured by collateral on which the lender has put in place a ‘first lien’ or legal right to secure the payment of debt. The further down the capital structure a security is, the higher the risk of ultimate loss.

The importance of quality bonds

A bond issuer’s ability to pay its debts (i.e. to make all interest and principal payments in full and on schedule) is a critical concern for investors. Most corporate bonds are evaluated for credit quality by credit rating agencies, such as Standard & Poor’s, Fitch Ratings and Moody’s Investors Service, and result in a rating on a standard scale that can be compared across issuers. These ratings scales are broadly split into two categories to reflect safer securities – referred to as “investment-grade” – and riskier securities – referred to as either “speculative-grade” or “high-yield”.

The financial health of the company or government entity issuing a bond affects the bond’s yield and subsequently the price investors are willing to pay. If the issuer is financially strong and investors are confident that the issuer will be capable of paying the interest on the bond and pay off the bond at maturity, then the yield will be lower as the perceived risks are lower.

High-yield corporate bonds on the other hand have lower, speculative-grade credit ratings than their investment-grade brethren. The greater risk of loss implied by these lower ratings, leads to higher yields compared with those seen within investment-grade corporate bonds. This is because there is a higher probability that a borrower defaults or fails to meet its obligation to make full and timely payments of principal and interest. Historically, speculative-grade companies experience higher default rates throughout economic cycles – and particularly so during recessions – resulting in potentially significant losses to investors when these occur.

Liquidity and volatility

High-yield bond funds tend to invest in loans, corporate bonds and structured credit which are at the riskier end of the investment universe. These types of securities can be difficult to buy or sell as they do not trade frequently, making them less liquid than investment-grade bonds. Bond funds where the underlying investments are investment-grade rated typically provide investors with daily liquidity as the market for these assets is larger, better-known and therefore more liquid. This is most prevalent when markets are volatile and investors are searching for “safer” assets, and when market pricing tends to be very reactive to liquidity and volatility risks.

High-yield bond funds can often have returns that behave similarly to equity markets; in other words, their returns often move in the same direction as equity markets. This is due to the capital price impacts of movements wider in credit spreads; namely the size of the bond yield margin above a risk-free asset yield which compensates investors for the associated credit risk. Typically, a credit spread reflects the difference in yield between a treasury and corporate bond of the same maturity.1

When credit spreads widen, this is a reflection that the market for those securities is requiring higher compensation for the underlying risk of holding those securities – for instance, for a higher risk of default, or more compensation for liquidity risk.

In times of heightened volatility, these dynamics can become self-reinforcing, given the right conditions. For instance, investors observing the capital value of their investment falling (as risks are increasing) may attempt to sell their exposure. If enough investors attempt to sell the same assets into a liquidity-constrained environment, this can exacerbate the issue, causing further losses – and in extreme circumstances, can cause a fund to “lock-up”, or result in capital being unable to be returned to investors in a timely fashion.

All investors have a different risk-return appetite; however, investors need to be mindful that economic growth has been reasonably solid for much of the past decade, and an environment where yields have been pushing progressively lower creates an environment where liquidity and volatility risks may not be appropriately priced in some markets. Funds with larger exposures to credit investments of lower-quality or greater complexity are likely to exhibit a higher likelihood of drawdowns on capital, and the potential for negative returns.

The final word

The ‘lower-for-longer’ interest rate theme continues to dominate markets, and low yields are likely to see low returns from bonds for a period of time. Investors moving into lower-quality high-yield bonds, should consider whether the additional yields on such bonds adequately offset the higher capital volatility and liquidity risks that come with them.

A retiree, or someone heading into retirement typically needs an investment strategy designed to provide a predictable and reliable income stream throughout their retirement years so if you’re not comfortable with capital volatility, lack of liquidity and you require a regular reliable monthly income stream, then a high-yield bond fund may not be the best choice for you.

There are many options along the risk curve when it comes to fixed income, with cash at the least risky end and instruments such as hybrids that also have equity characteristics at the other end. In other words, there is a wide spectrum of fixed income investments and it pays to understand what these are, the risks they have and how they can help meet set goals when building the fixed income component of a portfolio.

1 https://www.investopedia.com/terms/c/creditspread.asp

Author: Nathan Boon, Sydney, Australia

Source: AMP Capital 12th Nov 2019

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.